Why pre-planning with properly structured coverage can help families avoid forced sales, costly borrowing, and value destruction when taxes come due.

By Thomas J. Perrone, CLU, CIC

If most of your wealth is tied up in real estate, a family business, or long-term investments, your estate can be “asset-rich but cash-poor.” The challenge is that estate taxes and transfer costs can come due quickly—often before heirs have time to sell assets thoughtfully or arrange financing

The overlooked question in estate planning

For many business owners and high-net-worth families, estate planning focuses on what will be transferred and to whom. Just as important is the practical question that determines whether a plan works in real life: Where will the cash come from to pay estate taxes and other transfer costs—on time?

The issue is rarely a lack of wealth. It’s a lack of liquidity—and a very real deadline.

One of the most effective ways to solve this problem is also one of the most misunderstood: using life insurance to fund estate taxes and transfer expenses efficiently, without forcing the sale of long-term assets.

The real problem: a deadline and a liquidity crunch

Estate taxes and transfer costs are not optional—and they don’t wait. In many cases, they must be paid within nine months of death.

That timeline can create a liquidity crunch when a large share of an estate is tied up in:

- Real estate

- Privately held businesses

- Illiquid investments

When the calendar and the balance sheet don’t line up, families can be pushed into expensive decisions at exactly the wrong time.

Four ways estates typically cover the bill

Most estates end up using one (or a combination) of the following approaches to cover taxes and transfer costs.

1) Cash on hand

It’s simple—but it can be inefficient. Holding large amounts of cash can mean giving up long-term growth and flexibility. For many families, keeping millions in low-yield accounts “just in case” isn’t realistic.

2) Forced sale of assets

When liquidity isn’t available, families may have to sell assets quickly to meet the nine-month deadline.

Imagine being forced to sell:

- A commercial property

- A family business

- Land or long-held investments

…all on a tight timeline.

That can lead to a fire sale—assets sold below market value—eroding wealth that may have taken decades to build.

3) Financing the tax bill

Another option is borrowing money to pay the estate taxes.

Borrowing can preserve assets, but it introduces new risks and costs, including:

- Interest costs

- Long-term debt obligations

- Uncertainty around loan approval

Financing may preserve assets, but interest and repayment terms can drive the total cost well beyond the tax liability. And credit availability can tighten at exactly the wrong time.

4) Life insurance (a strategic liquidity solution)

This is where planning changes everything.

When life insurance is owned by a properly structured trust, it can create liquidity exactly when it’s needed—without disrupting the investment portfolio, the business, or the family’s long-term plan.

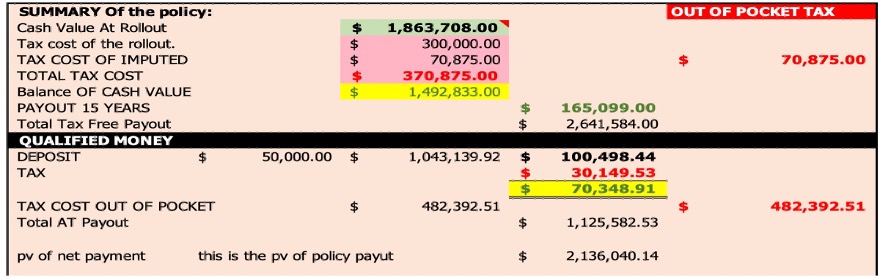

A real-world example

Consider this scenario:

- Age: 59

- Net worth: $15.5 million

- Projected estate value: $46 million

The estimated tax bill: $18.6 million due within nine months.

Now compare the cost of each strategy:

- Cash: forfeits future earning potential on the dollars held back

- Forced sale: can exceed $20 million when assets must be sold at a discount

- Financing: approximately $23 million over time, depending on rates and terms

- Life insurance: about $4.8 million in total cost in this example

That’s roughly 74% less expensive than the next best option.

Why life insurance often comes out ahead

Life insurance stands out for several key reasons:

Cost efficiency

Properly designed coverage can provide required liquidity at a fraction of the cost of holding idle cash, selling assets under pressure, or borrowing.

Tax advantages

- Death benefits are generally income tax-free

- Can be structured outside the taxable estate

Predictability

Unlike market-based holdings, a policy’s death benefit is designed to be available on a known event, with no market-timing risk.

- No volatility

- No timing risk

- Guaranteed payout when needed

Potentially strong effective returns

Depending on age, underwriting, and product design, the internal rate of return on a death benefit can be attractive (often cited at 10%+ in illustrations), with a potentially higher tax-equivalent return depending on your bracket.

The power of pre-planning

One of the most important insights is this:

Life insurance isn’t just an expense—it can be a pre-funded liquidity solution.

With current tax laws, individuals may have the ability to:

- Gift funds into a trust

- Avoid gift taxes within certain limits

- Systematically fund a future tax obligation

This transforms a reactive problem into a proactive strategy.

Final thoughts

Estate planning isn’t just about transferring wealth—it’s about preserving it.

Without proper planning, families may be forced into:

- Selling valuable assets

- Taking on debt

- Losing a significant portion of their legacy

Life insurance offers a smarter alternative:

- Lower cost

- Greater certainty

- Minimal disruption to your estate

Bottom line

If you expect your estate to face taxes or transfer costs, the real question isn’t if you’ll pay—it’s how.

And as the numbers clearly show:

For many families, life insurance is often the most efficient way to do it.

Work with your estate planning attorney, CPA, and insurance advisor to model the expected estate tax exposure, test different liquidity strategies, and determine whether a trust-owned policy fits your objectives and timeline.

WordPress notes (optional): Meta description: Estate taxes can be due within nine months, creating a liquidity crunch for families with illiquid assets. Learn four common strategies—and why trust-owned life insurance can be a cost-efficient solution.

Suggested slug: life-insurance-estate-tax-liquidity

Download your free report: The Big Beautiful Bill Tax Change Guide – this guide will help you understand all the opportunities this tax bill has offered to business owners.