Since 2017 the SPOUSAL LIFETIME ACCESS TRUSTS (SLAT) have been an exceptionally good planning tool, and a popular one in sheltering the growth of assets from estate taxation.

With the event of up and coming “the sunset” in 2026, more attention has been given to using this planning tool.

In this video, I discuss not only what a SLAT is, and how it is used, but bring into play the arbitraging of life insurance, and the powerful results from using it.

It is suggested that the planner learn as much as possible about the use of the SLAT. Also, the planner should work with a qualified attorney when presenting and implementing this planning technique.

Connelly was a hard case to digest as most of us who have been around the planning world for an exceptionally long time. We took the consequences of funding a stock redemption agreement as very normal. As normal as “cutting the end of the ham first.”

We are now forced to rethink this situation after the ruling, care must be taken when arranging the Buy and Sell Agreement and funding of a company, to avoid the results we have seen in Connelly.

Today I will bring you through a few options that advisors and business owners may consider when planning the transition of business interests.

CLICK HERE; YOUR REPORT WILL DOWNLOAD IMMEDIATELY!

After the 2017 Jobs Act, many of us (estate and business planners), had to shift our planning topics to moderate estate, Medicaid and income tax planning.

Many of the tools we used prior to the 2017Jobs Act were often used in the planning process, simply because more business owners were affected and exposed to the Federal and State Estate Tax System. Consequently, more sophisticated strategies were needed to shift value, freeze value, or shelter value from the estate.

Once the Jobs Act came into play, the exemption amounts eliminated many small business owners from the problem of estate taxation.

However, with part of the Jobs Act heading for Sunset, we may see more businesses becoming exposed to Federal and State estate taxation.

Time to go to the shed if you want to play in this market.

This video will help guide you to some of the areas of planning you will have to dust off and rekindle for use.

Download your Free Business Guide which will help explain many of the topics discussed. Immediate download, CLICK HERE!

An executive bonus arrangement is a method of compensating selected key employees in which the employer pays the premiums of a life insurance policy covering the employee’s life.

How the Plan Works

●Life insurance policy: The employee purchases, and is the owner of, a life insurance

policy on his or her own life. The employee retains – at all times – the right to name

the policy beneficiary and to receive the death benefit.

●Employer not a beneficiary: The employer cannot be the beneficiary, either directly or

indirectly, of the insurance policy.

●Written agreement: A written agreement provides for payment of a “bonus” in

exchange for the employee’s agreement to continue working for the employer. The

employer may also wish to pay a “double bonus” to help cover the employee’s

additional income tax liability.

●Premium Payments: The employer may make the premium payments directly to the

life insurance company, or the payments may be included in the employee’s paycheck,

with the employee paying the premiums.

●Tax treatment – employee: The employee includes in current income – and pays tax

on – the net premium paid by the employer.

●Tax treatment – employer: Subject to the “unreasonable compensation” rules, and as

long as the employer has no interest in the policy, the additional compensation is

deductible to the employer as an ordinary and necessary business expense.

Benefit to Employer

Benefit to Executive

Can reward selected key executives with varying coverage amounts.

The executive owns the policy. If he or she changes Employers, the policy is not lost.

Simple to implement, with little or no administration

Accumulated cash values can be used in emergencies, at retirement, or for personal costs investments.2

Premium costs are tax deductible.

Death benefit is generally received income-tax free.

Can be stopped without IRS approval or restrictions.

Proceeds may be used for estate settlement costs.

1 The discussion here concerns federal income tax law. State or local income tax law may vary.

2 A policy loan or withdrawal will generally reduce cash value and death benefits. If a policy lapses, or is surrendered with a

loan outstanding, the loan will be treated as taxable income in the current year, to the extent of gain in the policy. Policies considered to be Modified Endowment Contracts (MECs) are subject to special rules.

For a free report on Business Retirement Plans for Small Business Owners, click and submit. The report will be downloaded immediately. Learn how to use your cash flow to create tax-free wealth!

Since the exemption credit increased to a substantial amount a few years ago, the term “estate planning” took on a new meaning.

At one time estate planning was considered tax planning along with other aspects of planning of your estate, depending on whether you owned a business or not. Things like income for the family, debt payments, taxe reduction, income tax planning, and of course distribution of assets. There was always an emphasis on avoiding estate and state estate taxes.

However, as the exemption credit increased to the point that most American tax payers would be exempt, the emphasis change on how estate planning was done.

However, in 2025 the sunset provision will kick in and will redefine the estate planning landscape. The provision is set to go back to the exemption credit of about $600,000. However, most professionals feel it will be higher. Anyone’s guess.

With the possibility of lower exemption, estate planning will change. I personally feel small business owners will feel the impact more than most, as their business values will increase their potential exposure to Federal and State estate taxes.

Estate planning is an essential aspect of managing a small business. It can help ensure that your business is preserved as you want it to be, and that it can continue to operate smoothly even after you pass away. Part of estate planning for business owners will be to focus on the transition of the business more than before. If the exemption is lowered, small business owners will find themselves having to deal with a large tax at their death, upon the transfer of the business. Much can be avoided by doing planning now and using the exemptions available today.

Areas that need planning are:

Drafting a will and basic estate plan.

Planning for tax efficiencies.

Sorting out issues in family-owned businesses.

Drafting a buy-sell agreement (for multi-owner businesses).

Purchasing life and disability insurance.

Creating a succession plan.

Having a discussion with affected parties.

In order to have a proper discussion about estate planning the short video below will help you understand the main concept of asset distribution. If you are a small business owner, this information may be critical to your planning structure.

Request our FREE ESTATE PLANNING GUDIE FOR BUSINESS OWNERS:

For our FREE ESTATE PLANNING GUIDE FOR BUSINESS OWNERS, submit this short form AND the Estate planning guide will download immediately.

The Guide covers many of the areas you need to understand when doing your estate plan. It is also written in language you will understand.

Why do some Business Owners have higher costs than others when…

– They settle their estates…

– They retire…

– They transfer their business….

Let’s call the above items, “triggers”

Over the years I have had the experience of seeing the end results of the estate settlement process for many business owners. In many cases the results were not pretty because of the excess settlement costs. From my own experiences and case studies with associates, I have come to the realization that some business owners have higher estate transfer costs than other business owners. The interesting thing is the excess costs can be controlled by the estate owner.

Business owners usually have more value in their estates because of business values and settling the estate can be usually more complex. But as mentioned, in my opinion, there are controllable aspects of the costs and ways to mitigate these costs.

Estate transfers Cost: Three major reasons for higher costs!

No planning: This includes not having any plan, or not updating any earlier planning. Their estates are complex, and they need more than surface planning when their situation calls for more complex planning to carry out their goals. This takes more time and money. Without it they pay a price in estate settlement because they designed the wrong plan orhave no plan at all.

No time: In many cases, there isn’t any time to make changes. It is too late! All the changes should have been made in advance. Therefore, working on their business and estates yearly is a major benefit as opposed to waiting until it’s “too late”.

Owners don’t spend enough time asking the “what if’s” of their situations. Every year many changes come out of Washington that affect business and estate planning. Being unaware of these changes makes them vulnerable to excessive estate settlement costs. In many cases the business owner loses by default.

No liquidity: Settling the estate takes money. In many cases, most of the wealth is in the business and other personal hard assets which are difficult to turn into cash within a o brief period.

§ Even if they could be liquidated, they either run the risk of losing value, or causing major tax issues. Consequently, the estate is open until the taxes are paid and dissolution of assets is completed, causing major costs. Wealth gets stuck in business and its value is at the mercy of the market and other economic factors.

§ To prevent the lack of liquidity, we suggest that business owners use the business cash flow to create executive compensation plans with tax-free death benefits, and tax-free withdrawals. By doing this they create liquidity. When an estate owner dies, there is a guarantee that a tax-free death benefit will create the liquidity needed. Funded by the company cash flow.

Succession of the Business

No planning within the business for successor management. No building of a key group or key person to learn the business as an owner. Consequently , when the time for transition is near, there aren’t many options. This affects the “most potential value” of the business. The time to start planning transition of the business is when you start your business or buy a business! The key group is also the group that starts to define the culture of the business, making it easier to attract talented employees.

No systematizing of the business- the owner has not taken the time to prepare systems. Everything is in their heads, literally. There are no written down notes, no manuals or guides to pass on the instructions to others. “In simpler terms, the boss must be around for things to get done.” This limits the future ability to sell the business. Purchasers are looking to buy a business that has growth potential. Nor do purchasers in most cases want to invest in a company that has to restructure its operations. A purchaser is not likely to invest in a company where systems are not in place, and which are not transferable.

No development of “value drivers” to create growth and culture. Consequently, there is no culture, systems, and no middle management to take on responsibilities or a group to transfer the business to as mentioned above. This is a major issue with companies. A true test is asking the business owner if they can take 30 or more days off a year. If not, I tell them they have a job, but not a business. The owner of the business has not let go of the control they have of the business. It’s the business that controls the owner.

Retirement Planning and Why the Wrong Type Causes Chaos!

The wrong type of retirement plan- although qualified plans like 401k’s or profit-sharing plans are good for rank and file. They are not always the best retirement vehicle for high income business owners for a few reasons. Qualified plans are riddled with rules that business owners don’t need in their life. Qualified plans are needed in the company to attract employees, so in many cases, they are a particularly good method of attracting employees. However, for the business owner, Executive Compensation plans are more useful. Here are why qualified plans can be a thorn in the side of the high earning business owner:

No discretion as to who gets what amount in the plan-meaning the owner doesn’t get 100% of the distributed amount.

Who is to be in the plan- The owner can’t discriminate as to who should take part in the plan

No use of money 59 1/2 without penalty- Business owners are always looking for cash to support their businesses. The inability to withdraw funds from their retirement account is problematic when funds are needed

Age 72 RMD forcing high income owners to pay more taxes- business owners usually have other assets to rely on for income. It could be passive income from rents, income from the business and income from investments.

IRS in your life – Qualified plans need to file with IRS. However, if business owners used executive compensation plans, this is something they could avoid.

Many business owners can use executive compensation programs to develop wealth outside of their businesses and get great tax efficiency. For example, using a “Corporate Equity Executive Plan” will allow the owner of a company to use the company cash flow, pay 10% of the tax they would pay under a pension plan, and create a tax-free family bank. The family bank allows the owner to use the money, tax-free, any way they wish. Also, they are not forced to take the money out when they are retired.

For more information about business planning, I am offering YOU A FREE copy of my eBook, “Unlocking Your Business DNA” FREE Business guide which will help you understand some of the planning concepts used in retirement planning, business succession and estate planning. CLICK HERE for your free download. Your book will be downloaded automatically.

It is quite common for an employer to think in terms of a qualified retirement program when they think of retirement. The benefits of having a company plan would be tax-deductibility, tax deferred, an employee benefit to help attract employees, and a host of other reasons to have one. Most companies should have a long-term retirement plan for their employees. Most accountants will normally jump on this idea because it is another tax deduction.

However, what is rarely discussed are the benefits that the owner of the company receives from the qualified retirement plan! In most cases, the qualified retirement Plan will not be the best choice for the owner of the company, for various reasons.

Here are a few disadvantages for the high-income business owner:

Employer is the fiduciary is having responsibility and accountability to the plan (what happens when the employee loses money in the market?)

After-tax cost and non-recovery of the net outlay for the company

The percentage of payout for the employer is usually a much smaller percentage compared to the employees when they retire, so the employer owner is being discriminated against

The withdrawal is 100% taxable on all the funds

Tax exposure and penalty for using the funds before 59 ½.

Forced distribution RMD

For the employee, having a 401k and/or profit-sharing plan is a great deal. They could have matched contribution’s ability also. It is probably one of the best ways for people to save for their retirement.

The business owner or highly paid executive has the problem of creating enough capital for retirement so it can produce enough income to narrow the gap between their final pay and retirement needs. In most cases, because of the limits imposed on qualified plans and the taxability of the withdrawals, the qualified plan will not be the answer.

High Earning Business Owners – it’s a different story!

However, for the high earning employer, this is not a great deal compared to other executive compensation plans the employer could be. implemented for them. There are several major pension destroyers for the employer when comparing retirement plans vs executive compensation plans.

Disadvantages of a qualified retirement plan to the “high earning business owner”, compared to using a CEEP!

Limited contribution amount

100% of withdrawal taxable at retirement – With a CEEP you control the contribution amount

Pre 59 1/2 with penalty.

Funds in a qualified contribution plan would be very hard to extract (hardship clauses)

Bottom line, when the employer needs funds to build inventory, buy equipment, payroll, retirement funds are not a source, however, in a private executive compensation plan, they would be.

With a CEEP you have access to funds without a penalty

Death benefit; limited to accumulated fund, and taxable in a pension.

With an executive compensation plan like the CEEP, the death benefits are tax-free and large

CEEP would have a large tax-free death benefit to finish the retirement that wasn’t even started, and the benefit would be tax-free

Deductible:

Contribution plans are tax deductible as the contributions are made, consequently showing a charge to earnings in the year of contribution.

CEEPs are balance sheet friendlyas a receivable asset with interest.

CEEPs can be cost recoverable for the company, while retirement contributions are not. The qualified pension contributions are normally tax-deductible when made, but not recoverable for the company.

With a qualified plan, you are forced to take RMD (Required minimum distributions)

With CEEP, you are not. CEEPS distributions are tax-free.

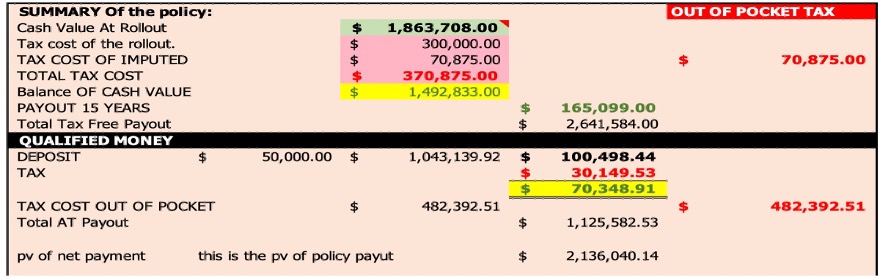

Table below: A qualified contributory plan doesn’t do the job when the owner of a company has an interest in growing wealth through their business. As mentioned, the contribution must be shared with the other employees, and there are rules as to the maximum contribution which high earners can make. In this case, the owner only could put the $30,000 in their account. With the CEEP Executive Compensation plan, the full $50,000 could be deposited into the account of the owner of the company!

Plan

Contribution

Future Value 66

Gross 15 payout

Taxes YRLY

Net Income

Qualified

30,000

893,351

80,348

24,104

56,244

CEEP

50,000

1,863,708

165,099

0

165,099

Many advisors including accountants, lawyers, and financial professionals are not aware of some of the great programs that can be designed using executive compensation. The CEEP program (Corporate Executive Equity Plan) is a flexible design built around the tax code.

Here is a chart comparing a Profit-Sharing Plan/401k and a specially designed CEEP Executive Compensation Plan.

ITEM

PROFIT SHARING 401K

CEEP

Tax deductible

Yes

Yes, optional

Tax deferred growth

Yes

Yes

Government Controlled

Yes

No

Selective as to Participants

No

Yes

Pre 59 1/2 availability

No

Yes

Tax Free withdrawal

No

Yes

Death Benefit

Only current accumulated value of account, taxable

Immediate substantial tax-free benefit

Required Minimum Distribution

Yes

No

Bottom line:

Contributory plans like 401k’s, SEPS, simple plans and IRA are wonderful plans for employees to save money for their retirement. However, given the above list of restrictions for employers, they are not effective for high income business owners in my opinion.

Note: I used 30% marginal bracket. Over a 15-year payout, the pension would have a $361,560 tax liability, while the CEEP was tax free.

To learn more about The Small Business Super Retirement Plan Just for Business Owners and High Earning Executives, request our free White Paper. CLICK HERE!

Over the years, I have been asked by business owners how they can use their company to create more tax deductions and to build retirement funds for themselves. When you put tax deductions and retirement funds in the same sentence, it suggests the vanilla response, of a pension plan of some type or a contributory retirement plan, like a profit-sharing plan, or a 401k.

However, is that what a business owner is really asking? Or, do they mean, they would like to build retirement funds through the business and assume they can get tax deductions? Or do both elements co-exist in the plan that they are thinking of? I think most advisors would suggest a 401k plan, a cash balance plan, a simple plan, or a profit-sharing plan for example.

This is what I call the costly, KNEE JERK REACTION.When asked by a business owner, about retirement plans, I have learned to slow it down and ask the business owner to clarify exactly what they are trying to accomplish, rather than rattle off a KNEE JERK response, such as a “profit sharing plan, or 401k plan”.

Questions like:

– Do you want to include everyone in the plan?

– Do you only want to favor yourself and family?

– Are you trying to give a benefit to a specific employee?

Do you want all the contributions to end up in your account, or are you willing to share with other employees? If so, how many and who?

If the employer/employee is trying to stockpile contributions to their account, they will have limitations with money purchase plans (limitations on contributions for 2022 of $58,000.) This makes it hard to deposit substantial amounts of money into the employer’s individual account, since they must include everyone.

Based on the response, this will determine how I design the plan. If he wants to spread the dollar among the group, you are talking about a qualified retirement plan. On the other hand, if they want limitations as to who can be involved, they are speaking about a non-qualified executive compensation plan.

In this model, I compared two scenarios so my client would have an idea of the difference in absolute dollars. I based the model on conservative values and returns, staying consistent with both types of plans. I am comparing a CEEP to a Hypothetical Pension plan (money purchase plan). [i]

As you can see in the chart below, based on the same parameters for each plan, the CEEP program created much more retirement benefits for the owner than a qualified retirement plan.

The owner participant received a much higher payout (tax-free), than the pension plan. In addition, if the owner died, from day one, the CEEP plan would pay a substantial tax-free amount to the family, while the qualified plan would only pay what was in the account which would be taxable to the beneficiary. The CEEP death benefit would be 100% tax free and would not be required to be withdrawn at death, or older ages like a pension or IRA plan would.

Once you compare a CEEP to the Pension plan, you can then see why defining exactly what the owner wants to accomplish is important as both plans offer different benefits and different tax scenarios.

KNEE JERK advice happens more than you think! And when it does, it can cost your client a lot of money, NOT to mention your reputation as an advisor.

In this case, the “Knee Jerk” suggestion to use a pension plan to solve the problem, shortchanged the business owner from having greater benefits for the future when compared to the suggested pension plan.

[i] In this scenario, the owner could only put in $30,000 of contribution out of the $50,000. Based on a five many company and different salary ranges.

REQUEST our free Business Essentials Report. This report is more than a report, it is a resource and guide to many planning ideas for business owners. It is an immediate download CLICK TO RECEIVE.

In my career I have experienced several business owners rushing through the implementation stages of designing their buy and sell agreement (BSA), probably one of the most important documents they will ever need, treating the process with little thought. As Rodney Dangerfield would say, “No respect”. When it was completed, it was very basic, doing more harm than good.

In some cases, maybe more than I think, the document being used by the drafting attorney was a “hand me down” from another attorney. While the “hand me down form” may have been useful in drafting another person’s situation and making it easier for the drafting attorney to do, it was not going to maximize my client’s planning situation.

In Paul Hood’s great book, “Buy And Sell Agreements, Last Will And Testament For Your Business”, he covers the consequences of not designing the right buy and sell agreement, and how important it is to spend the time and money preparing and designing this important document, with an experienced lawyer. [i]

Paul specifically speaks about attorneys using a “hand me down agreement”, and how it may be more harmful by having it than not.

The “Paul Hood Fire Drill”

He uses the idea of the “fire drill”. What happens when a “trigger happens? What will be the outcome and the consequences based on how your BSA is set up (or not set up), when you play it out. Like you were the leaving owner, and then again as the remaining owner. On a personal note, the “fire drill” advocated by Paul is something I use all the time and has been instrumental helping my clients and their attorneys in drafting the proper strategies for their situations. I have found that this has been a great way of helping my clients design the best BSA for themselves. It has allowed them to make it real and start developing questions and ideas that they can implement in their design. It keeps them involved with the process.

The “Fire Drill” strategy has put my clients in the “power seat” of knowledge, so when they discuss their BSA with their attorney, the elements and strategies that are being used are not foreign to them. This consequently helps them design a better BSA, reducing the time needed to spend with their attorney ($$$$$).

Keep in mind, many business owners start the process of designing the BSA when there has been no experience of consequences with an owner or co-owner leaving the company.

Everyone is Equal at the Start!

When owners design their BSA, they are all equal in status. People that enter into agreements want the agreement to favor them when a triggering event happens, even if the agreement has not been updated in years or there is no reference to the triggering event.

When are clients initially design their BSA, it probably will be one of the few times that all the partners will be negotiating with each other, because when there is a triggering event, chances are they will be negotiating with someone other than their co-owner.

The representative of the departing co-owner will have a different perspective as to what they want out of the BSA! Whether it is the spouse, their child, their law firm, whomever, they will be negotiating from a different point of interest.

Business relationships, and friendships are put aside. It is at this point you would hope your BSA covers all the areas of concern that need to be covered. The bottom line is the agreement must be exact as to what will specifically happen based on the triggering event. There is no room for errors if the document is specific. The best time to do this is when everyone is on equal ground.

For this reason, owners designing their BSA with their attorney should take it very seriously because they are really pre-negotiating for the people, they love the most without any certainty of which trigger will occur and which side of the trigger they will be on, leaving or a remaining co-owner.

It is extremely important that the triggering events be identified and that you will understand what will occur with each trigger event.

Paul Hood’s “fire drill” has made it easier for my clients to understand the importance of designing a solid BSA. By posing questions to the scenario, the BSA becomes very real to them.

Examples of how they would play out the “fire drill”

· What if you’re the first co-owner to leave?

· What if you’re the last remaining original owner?

· What if you end up with a co-owner you don’t want to be owners with?

· What happens if one of your co-owners, dies, divorces, or goes bankrupt?

By implementing your “fire drill”, you will start to formulate different scenarios for your own situation creating your own buy and sell design.

This is a critical document in keeping your business going should a trigger happen to any of the co-owners. Unfortunately, you must deal with it in advance and before there is a triggering event.

Risks when implementing your BSA:

· Using an attorney who is using a fill in the blank form.

· Not planning the scenarios before designing the plan.

· Not having a BSA.

· Not signing it.

· No dealing with how to fund such triggers.

There are so many elements to the buy and sell agreement that need to be covered, the planning of this document can’t be taken lightly. However, that is not to say you can’t have a great BSA. Having experienced professionals to help guide you through the process will pay off great benefits in designing and implementing your BSA.

We suggest you find competent counsel who has experience in designing the buy and sell agreements and discuss your goals and objectives with them.

If you would like our free Business Succession and Transition Planning Guide, click the link and we will send you a FREE WHITE PAPER to get you started. in your planning. YOUR FREE GUIDE

[i] E. Paul Hood is a prolific technical author. He has published a number of books on planning and is one of the leaders in estate planning and business succession planning.