Over the years, I have been asked by business owners how they can use their company to create more tax deductions and to build retirement funds for themselves. When you put tax deductions and retirement funds in the same sentence, it suggests the vanilla response, of a pension plan of some type or a contributory retirement plan, like a profit-sharing plan, or a 401k.

However, is that what a business owner is really asking? Or, do they mean, they would like to build retirement funds through the business and assume they can get tax deductions? Or do both elements co-exist in the plan that they are thinking of? I think most advisors would suggest a 401k plan, a cash balance plan, a simple plan, or a profit-sharing plan for example.

This is what I call the costly, KNEE JERK REACTION. When asked by a business owner, about retirement plans, I have learned to slow it down and ask the business owner to clarify exactly what they are trying to accomplish, rather than rattle off a KNEE JERK response, such as a “profit sharing plan, or 401k plan”.

Questions like:

– Do you want to include everyone in the plan?

– Do you only want to favor yourself and family?

– Are you trying to give a benefit to a specific employee?

Do you want all the contributions to end up in your account, or are you willing to share with other employees? If so, how many and who?

If the employer/employee is trying to stockpile contributions to their account, they will have limitations with money purchase plans (limitations on contributions for 2022 of $58,000.) This makes it hard to deposit substantial amounts of money into the employer’s individual account, since they must include everyone.

Based on the response, this will determine how I design the plan. If he wants to spread the dollar among the group, you are talking about a qualified retirement plan. On the other hand, if they want limitations as to who can be involved, they are speaking about a non-qualified executive compensation plan.

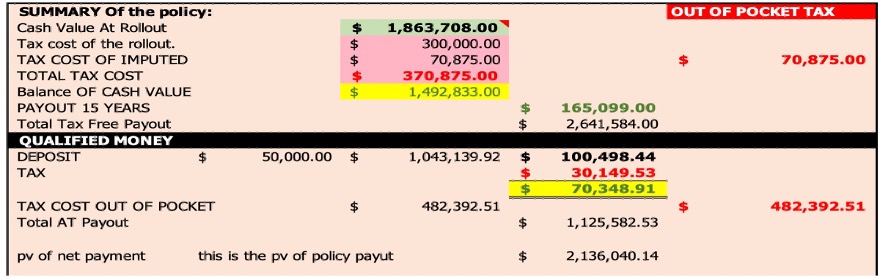

In this model, I compared two scenarios so my client would have an idea of the difference in absolute dollars. I based the model on conservative values and returns, staying consistent with both types of plans. I am comparing a CEEP to a Hypothetical Pension plan (money purchase plan). [i]

As you can see in the chart below, based on the same parameters for each plan, the CEEP program created much more retirement benefits for the owner than a qualified retirement plan.

The owner participant received a much higher payout (tax-free), than the pension plan. In addition, if the owner died, from day one, the CEEP plan would pay a substantial tax-free amount to the family, while the qualified plan would only pay what was in the account which would be taxable to the beneficiary. The CEEP death benefit would be 100% tax free and would not be required to be withdrawn at death, or older ages like a pension or IRA plan would.

Once you compare a CEEP to the Pension plan, you can then see why defining exactly what the owner wants to accomplish is important as both plans offer different benefits and different tax scenarios.

KNEE JERK advice happens more than you think! And when it does, it can cost your client a lot of money, NOT to mention your reputation as an advisor.

In this case, the “Knee Jerk” suggestion to use a pension plan to solve the problem, shortchanged the business owner from having greater benefits for the future when compared to the suggested pension plan.

[i] In this scenario, the owner could only put in $30,000 of contribution out of the $50,000. Based on a five many company and different salary ranges.

REQUEST our free Business Essentials Report. This report is more than a report, it is a resource and guide to many planning ideas for business owners. It is an immediate download CLICK TO RECEIVE.