Why do some Business Owners have higher costs than others when…

– They settle their estates…

– They retire…

– They transfer their business….

Let’s call the above items, “triggers”

Over the years I have had the experience of seeing the end results of the estate settlement process for many business owners. In many cases the results were not pretty because of the excess settlement costs. From my own experiences and case studies with associates, I have come to the realization that some business owners have higher estate transfer costs than other business owners. The interesting thing is the excess costs can be controlled by the estate owner.

Business owners usually have more value in their estates because of business values and settling the estate can be usually more complex. But as mentioned, in my opinion, there are controllable aspects of the costs and ways to mitigate these costs.

Estate transfers Cost: Three major reasons for higher costs!

No planning: This includes not having any plan, or not updating any earlier planning. Their estates are complex, and they need more than surface planning when their situation calls for more complex planning to carry out their goals. This takes more time and money. Without it they pay a price in estate settlement because they designed the wrong plan or have no plan at all.

No time: In many cases, there isn’t any time to make changes. It is too late! All the changes should have been made in advance. Therefore, working on their business and estates yearly is a major benefit as opposed to waiting until it’s “too late”.

Owners don’t spend enough time asking the “what if’s” of their situations. Every year many changes come out of Washington that affect business and estate planning. Being unaware of these changes makes them vulnerable to excessive estate settlement costs. In many cases the business owner loses by default.

No liquidity: Settling the estate takes money. In many cases, most of the wealth is in the business and other personal hard assets which are difficult to turn into cash within a o brief period.

§ Even if they could be liquidated, they either run the risk of losing value, or causing major tax issues. Consequently, the estate is open until the taxes are paid and dissolution of assets is completed, causing major costs. Wealth gets stuck in business and its value is at the mercy of the market and other economic factors.

§ To prevent the lack of liquidity, we suggest that business owners use the business cash flow to create executive compensation plans with tax-free death benefits, and tax-free withdrawals. By doing this they create liquidity. When an estate owner dies, there is a guarantee that a tax-free death benefit will create the liquidity needed. Funded by the company cash flow.

Succession of the Business

No planning within the business for successor management. No building of a key group or key person to learn the business as an owner. Consequently , when the time for transition is near, there aren’t many options. This affects the “most potential value” of the business. The time to start planning transition of the business is when you start your business or buy a business! The key group is also the group that starts to define the culture of the business, making it easier to attract talented employees.

No systematizing of the business- the owner has not taken the time to prepare systems. Everything is in their heads, literally. There are no written down notes, no manuals or guides to pass on the instructions to others. “In simpler terms, the boss must be around for things to get done.” This limits the future ability to sell the business. Purchasers are looking to buy a business that has growth potential. Nor do purchasers in most cases want to invest in a company that has to restructure its operations. A purchaser is not likely to invest in a company where systems are not in place, and which are not transferable.

No development of “value drivers” to create growth and culture. Consequently, there is no culture, systems, and no middle management to take on responsibilities or a group to transfer the business to as mentioned above. This is a major issue with companies. A true test is asking the business owner if they can take 30 or more days off a year. If not, I tell them they have a job, but not a business. The owner of the business has not let go of the control they have of the business. It’s the business that controls the owner.

Retirement Planning and Why the Wrong Type Causes Chaos!

The wrong type of retirement plan- although qualified plans like 401k’s or profit-sharing plans are good for rank and file. They are not always the best retirement vehicle for high income business owners for a few reasons. Qualified plans are riddled with rules that business owners don’t need in their life. Qualified plans are needed in the company to attract employees, so in many cases, they are a particularly good method of attracting employees. However, for the business owner, Executive Compensation plans are more useful. Here are why qualified plans can be a thorn in the side of the high earning business owner:

- No discretion as to who gets what amount in the plan-meaning the owner doesn’t get 100% of the distributed amount.

- Who is to be in the plan- The owner can’t discriminate as to who should take part in the plan

- No use of money 59 1/2 without penalty- Business owners are always looking for cash to support their businesses. The inability to withdraw funds from their retirement account is problematic when funds are needed

- Age 72 RMD forcing high income owners to pay more taxes- business owners usually have other assets to rely on for income. It could be passive income from rents, income from the business and income from investments.

- IRS in your life – Qualified plans need to file with IRS. However, if business owners used executive compensation plans, this is something they could avoid.

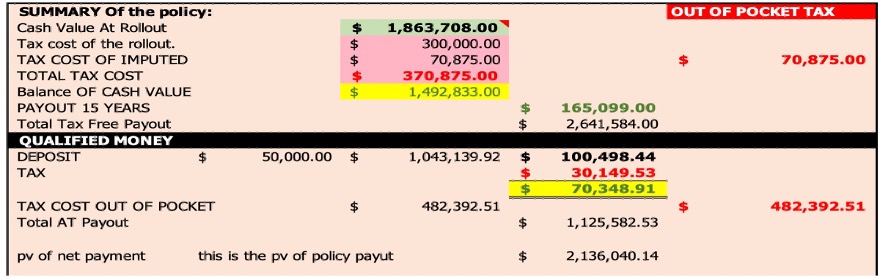

Many business owners can use executive compensation programs to develop wealth outside of their businesses and get great tax efficiency. For example, using a “Corporate Equity Executive Plan” will allow the owner of a company to use the company cash flow, pay 10% of the tax they would pay under a pension plan, and create a tax-free family bank. The family bank allows the owner to use the money, tax-free, any way they wish. Also, they are not forced to take the money out when they are retired.